Betterment Editors

Meet our writer

Betterment Editors

The editorial staff at Betterment aims to keep the Resource Center up to date with our evolving approach to financial advice, our product offerings, and new research. Articles attributed to the editorial staff may have originally been published under other Betterment team members or contributors. Read more detail on the Betterment Resource Center.

Articles by Betterment Editors

-

![]()

Investing in Your 30s: 3 Goals You Should Set Today

Investing in Your 30s: 3 Goals You Should Set Today May 31, 2024 9:23:32 AM It’s never too early or too late to start investing for a better future. Here’s what you need to know about investing in your 30s. In your 30s, your finances get real. Your income may have increased significantly since your first job. You might have investments, stock compensation, or a small business. You may be using or have access to different kinds of financial accounts (e.g. 401(k), IRA, Roth IRA, HSA, 529, UTMA). In this decade of your life, chances are you’ll get married, and even start a family. Even if you’ve taken this complexity in stride, it’s good to take a step back to review where you are and where you want to go. This review of your plan (or reminder to create a plan) is essential to setting up your financial situation for future decades of financial success. Don’t Delay Creating A Plan: Three Goals For Your 30s As always, the best thing to do is start with your financial goals. Keep in mind that goals change through time, and this review is an important step to make updates based on where you are now. If you don’t have any goals yet, or need some guidance on which investing objectives might be important for you, here are three to consider. Emergency Fund Sometimes your plan doesn’t go as planned, and having an adequate emergency fund can help ensure those hiccups don’t affect the rest of your goals. An emergency fund should contain enough money to cover your basic expenses for a minimum of three to six months. You may need more than that estimate depending on your career, which may or may not be one in which finding new work happens quickly. Also, depending on how much risk you want to take with these funds, you may need a buffer on top of that amount. Retirement Most people don’t want to work forever. Even if you enjoy your work, you’ll likely work less as you age, presumably reducing your income. To maintain your standard of living, or spend more on travel, hobbies or grandkids, you’ll need to spend from savings. Saving for your retirement early in your career—especially in your 30s–is essential. Thanks to medical improvements and healthier living, we are living longer in retirement, which means we need to save even more. Luckily, you have a secret weapon—compounding—but you have to use it. Compounding can be simply understood as “interest earning interest,”a snowball effect that can build your account balance more quickly over time. The earlier you start saving, the more time you have, and the more compounding can work for you. In your goal review, you’ll want to make sure you are on track to retire according to your plan, and make savings adjustments if not. You’ll also want to make sure you are using the best retirement accounts for your current financial situation, such as your workplace retirement plan, an IRA, or a Roth IRA. Your household income, tax rate, future tax rate and availability of accounts for you and your spouse will determine what is best for you. As you consider your goals, you may want to check out Betterment's retirement planning tools, which helps answer all of these questions. Also, if you’ve changed jobs, make sure you are not leaving your retirement savings behind, especially if it has high fees. Often, consolidating your old 401(k)s and IRAs into one account can make it easier to manage, and might even reduce your costs. You can consolidate retirement accounts tax-free with a rollover. If you have questions about your plan or the results using our tools, consider getting help from an expert through our Advice Packages. Major Purchases A wedding, a house, a big trip, or college for your kids. Each of these goals has a different amount needed, and a different time horizon. Our goal-based savings advice can help you figure out how to invest and how much to save each month to achieve them. Take the chance in your goal review to decide which of these goals is most important to you, and make sure you set them up as goals in your Betterment account. Our goal features allow you to see, track, and manage each goal, even if the savings aren’t at Betterment. -

![]()

Investing in Your 50s: 4 Practical Tips for Retirement Planning

Investing in Your 50s: 4 Practical Tips for Retirement Planning May 28, 2024 2:09:07 PM In your 50s, assess your retirement plan, lifestyle, earnings, and support for family. Practice goal-based investing to help meet your objectives. As you enter your 50s, you may feel like your long-term goals are coming within reach, and it’s up to you to make sure those objectives are realized. Now is also a perfect time to see how your investments and retirement savings are shaping up. If you’ve cut back on savings to meet big expenses, such as home repairs and (if you have children) college tuition, you now have an opportunity to make up lost ground. You might also think about how you want to live after you retire. Will you relocate? Will you downsize or stay put? If you have children, how much are you willing to support them as they enter adulthood? These decisions all matter when deciding how to strategize your investments for this important decade of your life. Four Goals for Your 50s Your 50s can be a truly productive and efficient time for your investments. Focus on achieving these four key goals to make these years truly count in retirement. Goal 1: Assess Your Retirement Accounts If you’ve put retirement savings on the back burner, or just want to make a push for greater financial security—the good news is that you can make larger contributions toward employer retirement accounts (401(k), 403(b), etc.) at age 50 and over, thanks to the IRS rules on catch-up contributions. If you’re already contributing the maximum to your employer plans and still want to save more for retirement, consider opening a traditional or Roth IRA. These are individual retirement accounts that are subject to their own contribution limits, but also allow for a catch-up contribution at age 50 or older. You may also wish to simplify your investments by consolidating your retirement accounts with IRA rollovers. Doing so can help you get more organized, streamline recordkeeping and make it easier to implement an overall retirement strategy. Plus, by consolidating now, you can help avoid complications after age 72, when you’ll have to make Required Minimum Distributions from all the tax-deferred retirement accounts you own. Goal 2: Evaluate Your Lifestyle and Pre-Retirement Finances When you’re in your 50s, you may still be a ways from retirement, however you’ll want to consider how to support yourself when you do begin that stage of your life. If you’ve just begun calculating how much you’ll need to save for a comfortable retirement, consider the following tips and tools. Tips and Tools for Estimating Income Needs Make a rough estimate of how much you spend on housing, food, utilities, health care, clothing, and incidentals. Nowadays, tools such as Mint® and Prosper include budgeting features that can help you see these expenditures. Subtract what you can expect to receive from Social Security. You can estimate your benefit with this calculator. Subtract any defined pension plan benefits or other sources of income you expect to receive in retirement. Subtract what you can safely withdraw each year from your retirement savings. Consider robust retirement planning tools, which can help you understand how much you’ll need to save for a comfortable retirement based on current and future income from all sources, and even your location. If there’s a gap between your income needs and your anticipated retirement income, you may need to make adjustments in the form of cutting expenses, working more years before retiring, increasing the current amounts you’re investing for retirement, and re-evaluating your investment strategy. Think About Taxes Your income may peak in your 50s, which can also push you into higher tax brackets. This makes tax-saving strategies like these potentially more valuable than ever: Putting more into tax-advantaged investing vehicles like 401(k)s or traditional IRAs. Donating appreciated assets to charities. Implementing tax-efficient investment strategies within your investments, such as tax loss harvesting* and asset location. Betterment automates both of these strategies and offers features to customers with no additional management fee. Define Your Lifestyle Your 50s are a great time to think about your current and desired lifestyle. As you near retirement, you’ll want to continue doing the things you love to do, or perhaps be able to start doing more and build on those passions. Perhaps you know you’ll be traveling more frequently. If you are socially active and enjoy entertainment activities such as dining out and going to the theater, those interests likely won’t change. Instead, you’ll want to enjoy doing all the things you love to do, but with the peace of mind knowing that you won’t be infringing on your retirement reserves. Say you want to start a new business when you leave your job. You’re not alone; more than a third of new entrepreneurs starting businesses in 2021 were between the ages of 55 and 64 according to research by the Kauffman Foundation. To get ready, you’ll want to start building or leveraging your contacts, creating a business plan, and setting up a workspace. You may also wish to consider relocating during retirement. Living in a warmer part of the country or moving closer to family is certainly appealing. Downsizing to a smaller home or even an apartment could cut down on utilities, property taxes, and maintenance. You might need one car instead of two—or none at all—if you relocate to a neighborhood surrounded by amenities within walking distance. If you sell your primary home, you can take advantage of a break on capital gains —even if you don’t use the money to buy another one. If you’ve lived in the same house for at least two out of the last five years, you can exclude capital gains of up to $250,000 per individual and $500,000 per married couple from your income taxes, according to the IRS. Goal 3: Chart Your Pre-Retirement Investment Strategy After you’ve determined how much you’ll need for a comfortable retirement, now’s also a good time to begin thinking about how you’ll use the assets you’ve accumulated to generate income after you retire. If you have shorter-term financial objectives over the next two to five years—such as paying for your kids’ college tuition, or a major home repair—you’ll have to plan accordingly. For these milestones, consider goal-based investing, where each goal will have different exposure to market risk depending on the time allocated for reaching that goal. Goal-based investing matches your time horizon to your asset allocation, which means you take on an appropriate amount of risk for your respective goals. Investments for short-term goals may be better allocated to less volatile assets such as bonds, while longer-term goals have the ability to absorb greater risks but also achieve greater returns. When you misallocate, it can lead to saving too much or too little, missing out on returns with too conservative an allocation, or missing your goal if you take on too much risk. Setting long investment goals shouldn’t be taken lightly. This is a moment of self-evaluation. In order to invest for the future, you must cut back on spending your wealth now. That means tomorrow’s goals in retirement must outweigh the pleasures of today’s spending. If you’re a Betterment customer, it’s easy to get started with goal-based investing. Simply set up a goal with your desired time horizon and target balance and Betterment will recommend an investment approach tailored to this information. Goal 4: Set Clear Expectations with Children If you have children, there’s nothing more satisfying than watching your kids turn into motivated adults with passions to pursue. As a parent, you’ll naturally want to prepare them with everything you can to help them succeed in the world. You may be wrapping up paying for their college tuition, which is no easy feat given that these costs – even at public in-state universities – now average in the tens of thousands of dollars per year. As your kids move through college, take the time to have a serious discussion with them about what they plan to do after graduation. If graduate school is on the horizon, talk to them about how they’ll pay for it and how much help from you, if any, they can expect. Unlike undergraduate programs, graduate programs assess financial aid requirements by looking at only the student’s assets and incomes, not the parents’, so your finances won't be considered. You’ll also want to set expectations about other kinds of support—such as any help in paying for their health insurance premiums up to a certain age, or their mobile phone plan, or even whether toward major purchases like a home or car. It’s great to help out your children, but you’ll want to make sure you’re not jeopardizing your own security. Your 50s may demand a lot from you, but taking the time to properly assess your investments, personal financial situation, lifestyle, and, if applicable, your support for children, can be truly rewarding in your retirement years. By tackling these four goals now, you can help set yourself up to meet your current responsibilities and increase your chances of a more financially secure and comfortable life in the decades to come. -

![]()

Welcome to Your 529 Education Savings Benefit

Welcome to Your 529 Education Savings Benefit Jun 5, 2023 2:10:14 PM Use this step-by-step guide to get started We’re excited you’re here and ready to get set up with a 529! You can enroll in a new 529 plan, select plan-specific investments, connect existing 529 accounts, and automate payroll deductions all within the Betterment app. Use the step-by-step guide below to get started. Setting up a new 529 Get started Log in to your account, and choose: Add new goal. Click on 529 Plan. Answer a few questions about your savings goals. Choose your 529 plan Betterment will display one or more 529 plans you might be interested in based on your location, your beneficiary’s age, and any income tax benefits that may be available to you. You can pick one of those, or review all other options. If you choose a plan that can be integrated within the Betterment experience, you’ll move on to the steps below. Note that integrated 529 accounts and their plans are not managed by Betterment and instead are held and managed by program administrators of each 529 plan. If your selected plan is not eligible to integrate, you can still access and connect it to Betterment manually, and take advantage of Betterment’s other products alongside your education savings account. Select a portfolio Within each plan, there are two types of investment options: Choose a portfolio that’s managed for you by the plan investment manager and automatically adjusts over time. Choose to manage your own portfolio to reflect your time frame and desired risk level. This option gives you more direct control. Enroll in a plan Complete paperwork: Confirm details about yourself and any beneficiaries. All set! Check out your new goal in your Betterment dashboard! Connecting an existing 529 account Get started Log in to your account, and choose: Add new goal. Click on the 529 Goal. Click on Connect an existing 529 (If you choose a plan that can be integrated within the Betterment experience, you’ll move on to the steps below. Note that integrated 529 accounts and their plans are not managed by Betterment and instead are held and managed by program administrators of each 529 plan. If your selected plan is not eligible to integrate, you can still access and connect it to Betterment manually, and take advantage of Betterment’s other products alongside your education savings account.) Tell us your account number. Read and sign our Terms and Conditions. Authorize Betterment to access your account. In the Betterment app, you will now see your 529 plan in your dashboard. Set up contributions Navigate to set up contributions or deposits. You have two ways to contribute toward your 529 account: through payroll deductions or by linking a bank account within Betterment: Payroll deductions (post-tax): These payments are eligible for an employer match, if your employer offers one. Select Payroll deduction to have contributions automatically come out of your paycheck. Choose a 529 account to contribute to. Decide how much money you want to contribute per pay period. Review and approve your contribution rate. Linked bank account: Select Linked bank account Choose a 529 account to contribute to. Decide how much you want to contribute and at what frequency. Review and approve your contribution rate. Dashboard overview Overview tab: View all of your 529 accounts and balances. Note that payments typically take 5-7 days to process. Activity tab: See your Betterment payment activity. Settings tab: See your 529 account details and link your Betterment account directly to your 529 plan account in order to navigate back and forth seamlessly. -

![]()

How to pick a 401(k) contribution rate

How to pick a 401(k) contribution rate Sep 22, 2022 10:08:00 AM Your 401(k) contribution rate - also known as a deferral rate or savings rate - is a key part of a successful retirement strategy. You’ve taken that first step and have set up your Betterment 401(k) account - well done! One important piece to consider next is your contribution rate - how much from each paycheck will go into your account? With your Betterment 401(k), you could use a percentage or a fixed dollar amount, whichever you prefer. Here are a few other things to consider: Were you automatically enrolled? Many employers choose to automatically enroll their employees in the plan with a default contribution rate of 3% – if you're not sure, please check with your employer or take a look in your Retirement goal. Keep in mind, whatever the default contribution rate is, it’s just a starting point. You can (and probably should) increase that contribution rate at any time in your account. At least a decade without a paycheck Most experts recommend contributing 10%–15% of your paycheck to have enough to last you through retirement - which could be 20-30 years considering how long people are living! If you retire at age 65, with a healthy lifestyle and no major risk factors, you could live well into your 80s or 90s. That means you'll want to set yourself up for living off your personal savings and investments for about 20 years! Starting small is better than nothing If 10-15% of your paycheck sounds absurd to you right now - deep breath, think of that as something to aim for. You can start with something smaller, maybe 5 or 6%, and slowly but surely increase your savings rate every year – your birthday? Give yourself a gift and increase it by 1%. Your work anniversary? Cheers to you, bump it up again. And those 1% increases can actually be a big deal. Go for the max Because of its tax benefits, the IRS sets a limit on how much you can put into your 401(k) every year. So you could aim to contribute as much as the IRS allows! For people 50 and over, the limit is higher, which is referred to as “catch-up contributions.” And if you really want to be an over-achiever, you can also contribute to an IRA, an individual retirement account, to save even more. Tax considerations With your Betterment 401(k), you can make contributions into a traditional 401(k) account and/or a Roth 401(k). There are tax benefits to both: Traditional 401(k): Contributions are deducted from your paycheck before taxes are withheld, which can lower your taxable income. Both your contributions and investment earnings are “tax-deferred,” meaning you won’t pay taxes on what you contributed to the account as well as any earnings until you withdraw the money at retirement. In other words, save on taxes now, pay taxes later. Roth 401(k): Contributions are made with after-tax dollars so your withdrawals—both the contributions and earnings—are tax-free once you decide to retire (minimum age, 59½), and as long as you’ve held the Roth account for at least five years. In other words, pay taxes now, no taxes later. Remember that you can use both! Say you want to contribute 10% towards your retirement? You can put 5% into a traditional 401(k) and 5% into the Roth 401(k). This is one way you can balance your tax exposure. If you already have your account set up, log in today to adjust your contribution rate or reassess your traditional and Roth contributions. Haven’t started saving in your Betterment 401(k) yet? Check your email for an access link from Betterment, or get in touch: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET -

![]()

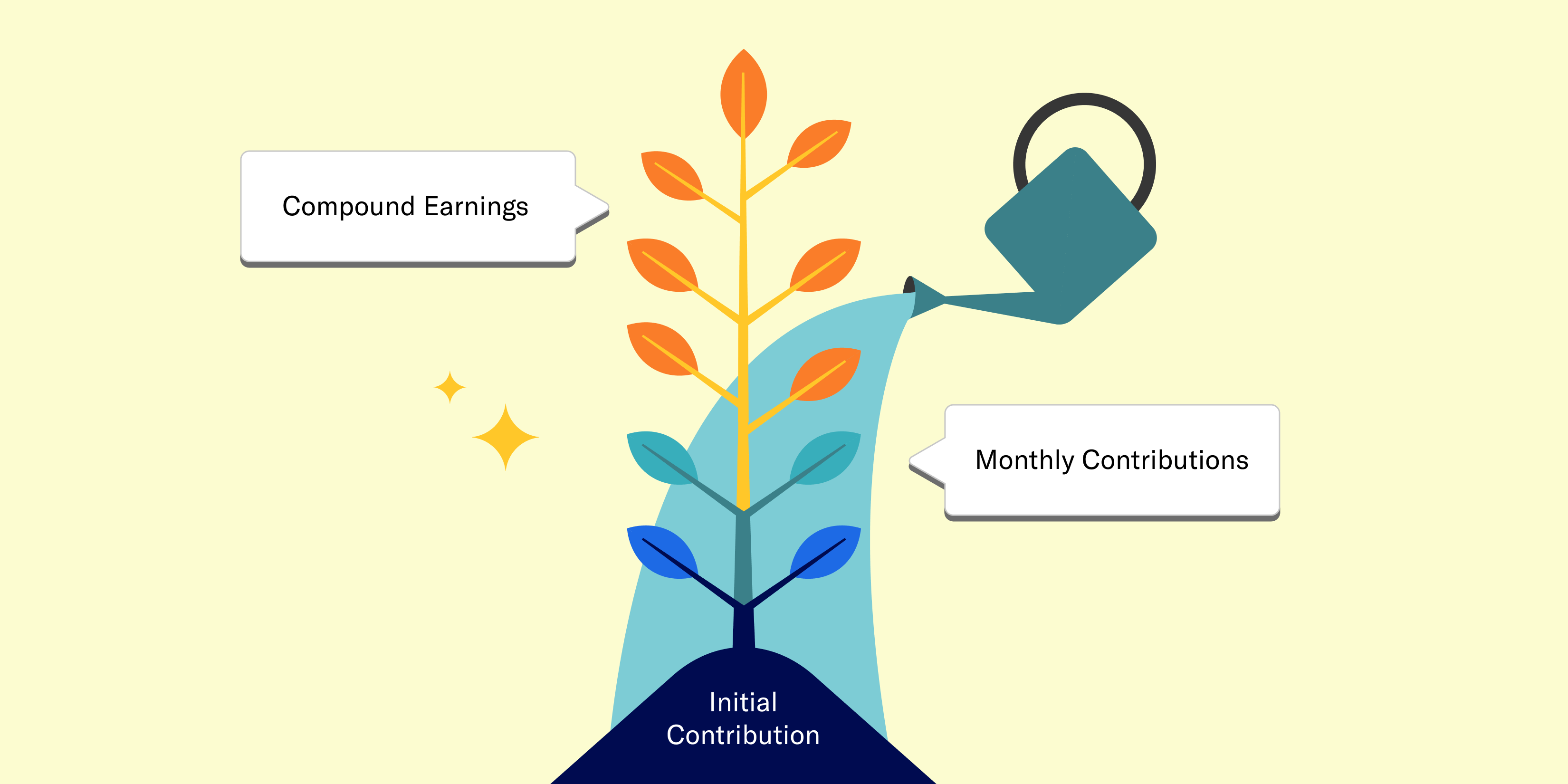

When’s the best time to invest for retirement? Now.

When’s the best time to invest for retirement? Now. Sep 21, 2022 4:42:00 PM Should you start saving for retirement? Unless you are on one of those richest-people-in-the-world lists - then the answer is, most likely, yes. From paying the rent or mortgage, credit card bills, student loans, daily living expenses - there are a lot of things competing for your money’s attention! The idea of saving for retirement can easily be pushed to the backburner for all of those other - completely understandable! - reasons. But we’re here to say - hold the phone. Even a little bit into a 401(k) can make a huge difference for your retirement. Rock and roll When a rock rolls down a hill, it goes faster and faster on its way down. It has something to do with momentum and physics – we’re not scientists here, we’re investment professionals. But the same concept applies to your 401(k) - not because of physics, but because of compounding interest. Compounding interest means that not only are your original dollars growing based on potential stock market gains, but that newly earned money also grows whenever the stock market goes up! Give compounding time to shine If the magic of compounding interest isn’t enough to get you going right away, there is one other factor to consider. If someone starts saving 6% of their paycheck at age 25, they are expected to end up with more money at age 65 than someone who contributes 10% starting at age 40. And here’s the real kicker - the person who’s doing 10% starting at age 40 will put in more of their own dollars, and is still expected to end up with less by the time they reach age 65. How is that possible? The 6% contributions had more time to grow – more time to roll down that hill gathering speed – or in this case – money. If you already have an account, log in today to view your contribution rate and consider giving it a bump – even a 1% increase can make a difference in your retirement years! Haven’t started saving in your Betterment 401(k) yet? Check your email for an access link from Betterment, or get in touch: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET -

![]()

Getting started with your Betterment 401(k)

Getting started with your Betterment 401(k) Sep 21, 2022 1:41:00 PM Your employer chose Betterment as its 401(k) provider - so come on in and be invested for your future. Traveling around the world. Taking up a new hobby. Spending more time with family and friends. Whatever your retirement dreams are, a 401(k) can help you make them a reality. And luckily for you, your employer chose Betterment to manage its 401(k) plan. Top 3 perks of a 401(k) Participating in your employer’s 401(k) plan is a good idea for many reasons – here are the top three. With a 401(k), you can: Contribute via convenient, automatic payroll deductions (one less thing to think about!). Save on taxes, whether those savings happen today with a traditional 401(k) or at retirement with a Roth 401(k) (and the cool thing is that you can use both!). Invest more than with other retirement vehicles (individual retirement accounts (IRAs) have lower caps on how much you can put in). All said, saving for retirement with a 401(k) is basically a no-brainer. Without a regular paycheck in retirement, you’re going to rely on your own savings. And we’re not talking about cash-under-the-mattress savings or even safe-in-the-bank savings - but invested savings, which is what you get with a 401(k). (Why is it so critical to invest for long-term goals, rather than simply saving money in the bank? To tackle one word: Inflation.) Top Betterment features Betterment offers several features to help you pursue your retirement goals: Goal based – Your 401(k) will automatically be a “Retirement” goal on the Betterment platform (you could add additional goals for other things if you want). Our goal-based platform looks at your timeline until retirement and the desired amount you want to save, to help you invest in an expert-built portfolio. Low cost – Our approach uses low-cost exchange-traded funds (ETFs) so more of your money stays invested in your account. High tech –Certain portfolio strategies and goal types are automatically rebalanced and adjusted over time, and our tax-smart tools are available to you at no added management fee. Personalized – Betterment helps you work towards your long- and short-term financial goals with personalized advice. It’s easy to get started Betterment will contact you via email to set up your account via a secure link that’s unique to you. If you haven’t received an invitation from us to set up your account, please contact us. Once you’ve set up your account, be sure to set a contribution rate to help you pursue your goals (although starting with anything is far better than nothing!) and you’ll want to initiate a rollover of any old 401(k)s into your new Betterment 401(k). Were you automatically enrolled in your plan? If so, you still need to set up your account with a username and password. If your employer has determined an automatic contribution rate for your organization, know that you can adjust this in your account at any time. Betterment strives to make saving and investing for retirement easy. But we know you still might have questions, so we’re here to help: Explore our 401(k) employee resources Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET -

![]()

Rolling over is more than a dog trick

Rolling over is more than a dog trick Sep 21, 2022 1:36:00 PM Three reasons why rolling over 401(k)s from former employers may make sense. Have money sitting in 401(k) accounts from former employers? If so, you’re not alone. Recent research estimates that there are more than 24 million “forgotten” 401(k) accounts, holding approximately $1.35 trillion dollars. Are any of those dollars yours? If so, you should consider rolling any old 401(k) into your new Betterment 401(k) – here’s why: 1. Get a comprehensive view of your retirement savings When you have accounts here, there and anywhere, it’s hard to get a handle on where you stand. By rolling them over to your Betterment account and consolidating your retirement assets in one place, you can ensure your portfolio is appropriately diversified, monitor your progress, and rest assured that your investments aren’t competing or canceling each other out. 2. Avoid fees! Every 401(k) plan comes with fees. If you have multiple 401(k)s, you are paying fees for all of those accounts! Betterment has fees too –but we use low-cost exchange-traded funds (ETFs) in our portfolios, helping to keep fees low. 3. Access personalized financial advice and service Whether you want to talk investment strategy or review your retirement account, Betterment has CERTIFIED FINANCIAL PLANNER™ professionals and a customer support team that’s easy to reach when you need them. Your plan may include complimentary access to our team of CFPs® or you can book a call for a one-time fee. Other options Since you have access to a Betterment 401(k) through your employer, it could make sense for you to roll old 401(k)s into your Betterment 401(k) for all the reasons outlined above. But you do have other options: Leave it where it is. Roll it into an IRA (Individual Retirement Account), either with Betterment or another financial institution. Cash it out – this will come with taxes and potentially fees, and your money will no longer be invested (and potentially growing) for your retirement. Ready to roll? In just a few clicks, you can start the rollover process to Betterment and be set up with an appropriate investment strategy for you. You’ll receive a personalized set of rollover instructions via email, with no paperwork required by us. Have a different kind of account to roll over? No problem. You can roll over your IRAs, pensions, 401(a)s, 457(b)s, profit sharing plans, stock plans, and Thrift Savings Plans (TSPs) to Betterment using the same simple process. If you've already claimed your account, you can click here to start your rollover. If you have any questions along the way, our team is ready to help: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET -

![]()

What is a Required Minimum Distribution?

What is a Required Minimum Distribution? Sep 15, 2022 4:47:00 PM In exchange for all of the tax advantages 401(k)s provided during your accumulation years, by law, you will need to start taking distributions from your account when you turn 72. 401(k) plans can help you save for retirement in a tax-advantaged way. However, the Internal Revenue Service (IRS) requires that you start taking withdrawals from their qualified retirement accounts when you reach the age 72. These withdrawals are called required minimum distributions (RMDs). Why do I have to take RMDs? In exchange for the tax advantages you enjoy by contributing to your 401(k) plan, the IRS requests collection of taxes on these amounts when you turn 72. The IRS taxes RMDs as ordinary income, meaning withdrawals will count towards your total taxable income for the year. Generally, the IRS collects taxes on the gains in retirement accounts such as 401(k)s. However, if Roth 401(k) account assets are held for at least 5 years, Roth 401(k) funds are not taxed. Because there are taxes being paid to the government, these distributions are NOT eligible for rollover to another account. How much do I have to withdraw? RMDs are calculated based on your age and your account balance as of the end of the previous year. To determine the required distribution amount, Betterment divides your previous year’s ending account balance by your life expectancy factor (based on your age) from the IRS’ uniform lifetime table. If you had no balance at the end of the previous year, then your first RMD will not occur until the following year. Additionally, if you have taken a cash distribution from your 401(k) account in any given year you are subject to an RMD, and that distribution amount is equal to or greater than the RMD amount, that distribution will qualify as the required amount and no additional distribution is required. Does everyone who turns 72 need to take an RMD? Turning 72 in a given year doesn’t mean that you have to take an RMD. Only those who turn 72 in a given year AND meet any of the following criteria must take an RMD: You have taken an RMD in previous years. If so, then you must take an RMD by December 31 of every year. You own more than 5% of the company sponsoring the 401(k) plan. If so, then you must take an RMD by December 31 every year. You have left the company (terminated or retired) in the year you turned 72. If so, then the first RMD does not need to occur until April 1 (otherwise known as the Required Beginning Date) of the following year, but must occur consecutively by December 31 for every year. Example: John turned 72 on June 1, 2022. John also decided to leave his company on August 1, 2022. He has been continuously contributing to his 401(k) account for the past 5 years. The first RMD must occur by April 1, 2023. The next RMD must occur by December 31, 2023 and every year thereafter. You are a beneficiary or alternate payee of an account holder who meets the above criteria. If you are 72 and still employed, you do NOT need to take an RMD. What are the consequences of not taking an RMD? Failure to take an RMD for a given year will result in a penalty of 50% of the amount not taken on time by the IRS. How do I take an RMD? Betterment will automatically process your RMD if we see that you are over age 72 and no longer actively employed with your employer. If you have the option to take an RMD - age 72 but still employed - your employer can provide you with a form to submit a request. If you have a linked bank account on file, the RMD will be deposited into that account; if we do not have a bank account on file, a check will be mailed to the address in your account.